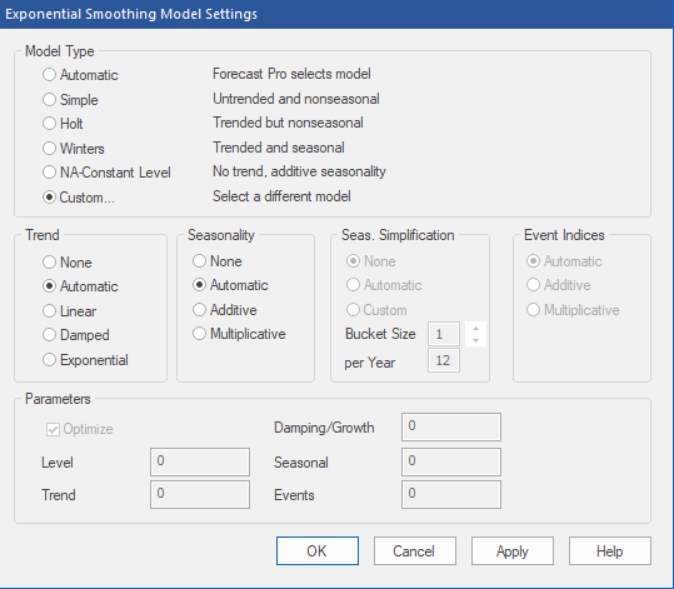

Selecting Custom on the Exponential Smooth icon drop-down on the Forecasting tab or selecting Forecasting>Exponential Smoothing on the Navigator context menu invokes the Exponential Smoothing Model Settings dialog box shown below.

If you are forecasting data where the periods per cycle is greater than 13 (e.g., weekly data) you can use the Seasonal Simplification options to reduce the number of seasonal indices to use. None instructs Forecast Pro to not use seasonal simplification. Automatic allows Forecast Pro to automatically select the number of indices using out-of-sample testing. Custom allows you to specify the number of indices by specifying the “bucket size” (i.e., how many periods to combine into each seasonal index) or by setting the number of indices to use per year. Note that seasonal simplification cannot be used in conjunction with event models.

The Event Indices section allows you to specify the form of the event indices (additive, multiplicative or let Forecast Pro decide). This section will only be available if you have specified an event schedule. When events are used in conjunction with a seasonal model, the form of both the event indices and seasonal indices must match—so the Event Indices section will also be greyed out if Seasonality is set to anything other than None.

The Parameters section allows you to set the smoothing weights to specific values. In general, this is not a recommended practice (allowing Forecast Pro to optimize the smoothing weights is recommended). If you do wish to set the smoothing weights, you must specify a specific form for the trend and seasonality.

When you click the OK button Forecast Pro will apply the appropriate modifier on the Navigator and build the specified model.

The exponential smoothing modifiers include:

\EXSM=XY. Use a custom exponential smoothing model with trend type X (N=no trend, L=linear trend, D=damped trend, E=exponential, *=Forecast Pro decides), seasonality type Y (N=nonseasonal, M=multiplicative seasonal, A=additive seasonal, *=Forecast Pro decides) and optimized smoothing weights.

\EXSM=XY(A,B,C,D). Use a custom exponential smoothing model with trend type X (N=no trend, L=linear trend, D=damped trend, E=exponential, *=Forecast Pro decides), seasonality type Y (N=nonseasonal, M=multiplicative seasonal, A=additive seasonal, *=Forecast Pro decides) and user defined smoothing weights (A=level, B=trend, C=damping/growth, D=seasonal).

\SS. Use Forecast Pro’s automatic identification procedure to determine whether to use seasonal simplification and the appropriate bucket size.

\SS=n. Use seasonal simplification with n periods for each seasonal index or “bucket”.